Digital lending has reshaped how Indian banks and non banking financial companies reach borrowers. The Reserve Bank of India Working Group on Digital Lending found that digital disbursements among sampled lenders grew from INR 11,671 Crores (approx. US$1.4 billion) in 2017 to INR 1,41,821 Crores (approx. US$17 billion) in 2020, a twelvefold rise that invited fresh regulatory scrutiny. On May 8, 2025 the RBI Digital Lending Directions, 2025 consolidated earlier guidance into one rulebook governing how loans are sourced, disbursed, and serviced. For Banking, Financial Services and Insurance (BFSI) firms, the opportunity is enormous, yet the compliance burden is real.

What Is Digital Lending?

Digital lending is the delivery of credit entirely through digital channels, where application, identity verification, underwriting, disbursement, and repayment happen online with minimal paperwork. It spans banks, non banking financial companies, and their technology partners, relying on data driven underwriting and electronic Know Your Customer (KYC) checks to turn a multi day process into one completed in minutes.

What Are the Biggest Compliance Challenges in Digital Lending?

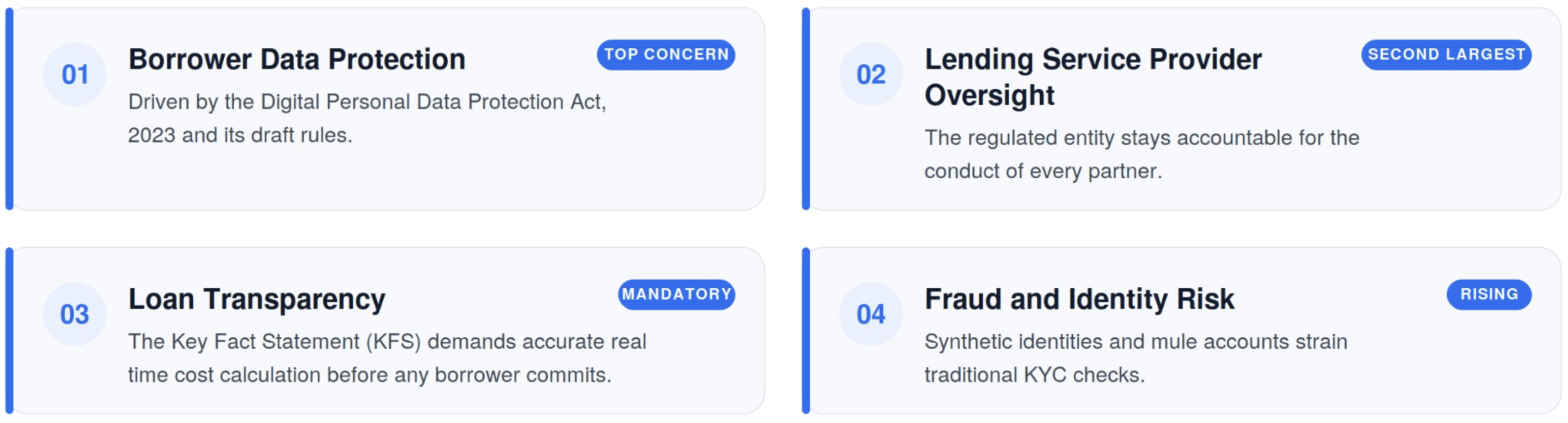

Indian lenders face pressure as regulation tightens. The market keeps expanding, with industry bodies reporting that member fintechs disbursed roughly INR 1,46,000 Crores (approx. US$17.5 billion) across nearly 10 Crore loans in FY24. That scale magnifies four core challenges.

Industry surveys consistently show that a majority of lenders cite compliance complexity as their primary barrier to scaling digital books. Penalties, reputational damage, and customer churn follow weak controls. The November 2023 increase in risk weights on unsecured consumer credit to 125% added further discipline to digital books. For BFSI leaders, governance can no longer be an afterthought bolted on after launch.

Building a Governance First Digital Lending Strategy

A sustainable digital lending operation starts with structure, not speed. Regulated entities must own the full customer journey even when partners handle origination. The 2025 Directions reinforced that all loan flows must pass directly between the borrower and the regulated lender, with no third party pooling accounts, and retained the Default Loss Guarantee cap at 5% of the portfolio.

Risk mitigation depends on auditable trails. Every consent, disclosure, and disbursement should be timestamped and instantly retrievable. The right platform converts these obligations into repeatable workflows, turning the framework from a constraint into an operating standard that protects both lender and borrower.

Which Capabilities Define a Modern Digital Lending Platform?

Technology decides whether compliance scales or breaks under volume. The following capabilities are required for Indian BFSI institutions that need dependable, audit ready infrastructure.

• Real time KYC verification: Instant identity validation against Unique Identification Authority of India (UIDAI) Aadhaar and PAN records, cutting onboarding fraud.

• Automated Key Fact Statement generation: Accurate Annual Percentage Rate and fee disclosure produced before disbursement.

• Account Aggregator integration: Consent based data sharing through the Reserve Bank approved Account Aggregator framework, improving underwriting without storing raw data.

• End to end encryption: Information secured in transit and at rest, aligning with Digital Personal Data Protection Act, 2023 obligations.

• Real time compliance monitoring: Continuous surveillance of partner conduct, disbursement flows, and reporting deadlines.

• AI and Machine Learning risk scoring: Behavioural and alternative data models that sharpen credit decisions and surface fraud early.

These features integrate with core banking systems and credit bureaus through secure Application Programming Interfaces (APIs).

Where Is Digital Lending Headed Over the Next Two Years?

The trajectory favours institutions that treat compliance as infrastructure. Research estimates for India's digital lending market range from around US$515 billion to nearly US$1.3 trillion by 2030, with embedded finance and co lending driving the next wave. Organizations are increasingly emphasising regulatory technology that automates oversight rather than expanding manual teams. Forward thinking lenders will explore alternative data underwriting, deeper Account Aggregator adoption, and tighter LSP governance. Those that build trust through transparent, secure lending earn lower default rates and stronger loyalty. Early adopters of automated compliance report faster onboarding and fewer regulatory observations, a measurable competitive edge. The lenders who win will not be the fastest to launch, but the most disciplined in how they scale.

How Landmark Systems and Solutions Powers Compliant Digital Lending

Building a digital lending business means putting safety and rules first. DigiLending by Landmark Systems and Solutions is a simple, all-in-one platform that helps Indian financial institutions easily follow strict RBI rules while growing safely. It checks customer identities instantly using Aadhaar and PAN, safely reviews financial data without storing it, and automatically creates clear fee statements for borrowers. By handling the stressful paperwork and rule-checking automatically, DigiLending reduces onboarding friction, strengthens data protection, and keeps reporting audits ready, so your teams focus on lending instead of firefighting.

Connect with Landmark Systems and Solutions to assess your digital lending readiness and turn compliance into a lasting advantage.