What is Customer Onboarding in Financial Services?

Customer onboarding is the process of bringing new clients into a financial institution. It includes verifying their identity, collecting required documents, performing background checks, and finally activating their accounts. This process is critical because it sets the tone for the entire customer relationship.

Imagine onboarding like welcoming a guest to your home. A friendly security guard who asks a few basic details, like name and purpose, makes the entry quick and smooth. Ask too many questions and tell them to fill out a form, taking up a lot of time, and they might get frustrated and leave.

On the contrary, if there's no guard at all, anyone can walk in, leaving your home unprotected. This balance of security and ease is exactly what good onboarding aims for in financial services.

Think about it in various real-world scenarios. For instance, when opening a bank account, customers submit personal details like name and address. Then the staff collect your documents and perform identity checks to open savings or current accounts. Similarly, setting up a demat account for stock market investments requires verifying PAN and bank details to ensure safe trading. Loan setups work likewise; they need credit reviews and income proof to speed approvals.

In India, customer onboarding must comply with strict regulations set by the Reserve Bank of India (RBI). These regulations require financial institutions to perform Know Your Customer (KYC) checks to prevent money laundering and fraud. KYC verification confirms that customers are who they claim to be.

How Onboarding Used to Work: The Paper-Based Era

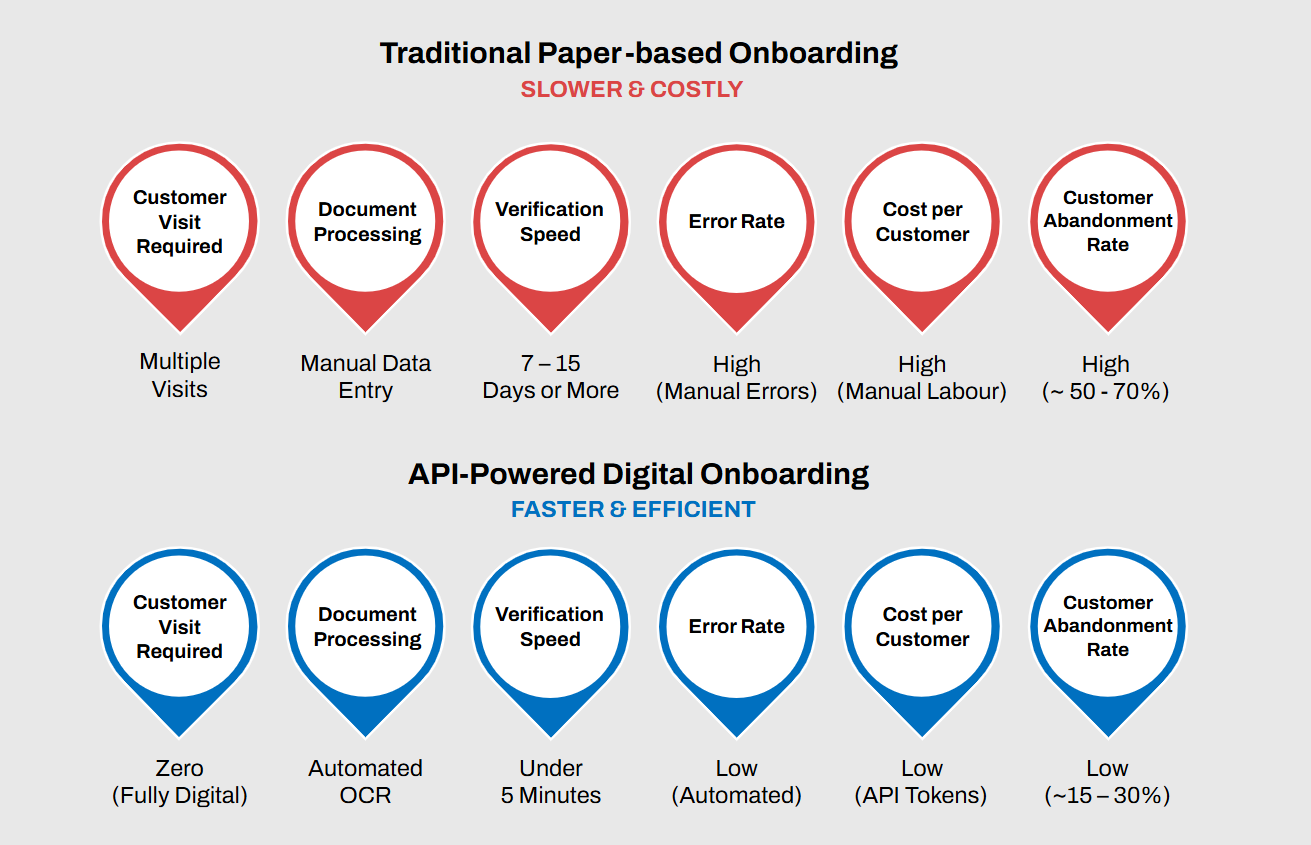

Traditional onboarding was a lengthy, paper-heavy process. Customers had to make multiple branch visits in person to fill out multiple forms by hand. They had to submit physical copies of identity documents like PAN cards, Aadhaar cards, and address proofs. Bank staff would then manually verify these documents against government databases.

This process could drag on for weeks, and it's no wonder many gave up along the way. Reports show that excessive paperwork and delays caused around 38% of potential customers to abandon their applications entirely, costing banks valuable opportunities and leaving people frustrated. The inefficiency was glaring, but change was on the horizon. Starting around 2016-2017, the rollout of Aadhaar-based eKYC began shifting things digital, backed by UIDAI and RBI support that quickly spread to banks, NBFCs, and mutual funds.

What is an API and How Does it Help?

So, what's an API, and why does it matter here? It is short for Application Programming Interface, a bridge that lets different software systems chat seamlessly. Think of it as a digital messenger that connects your bank's system with government databases, verification services, and customer-facing apps.

In the context of financial onboarding, APIs enable instant communication between banks, brokers, NBFCs and external data sources. When a customer enters their Aadhaar number, an API can instantly fetch and verify their details from the UIDAI database without any manual intervention. Similarly, PAN verification happens in real time through APIs connected to income tax databases.

Benefits of API-Powered Onboarding

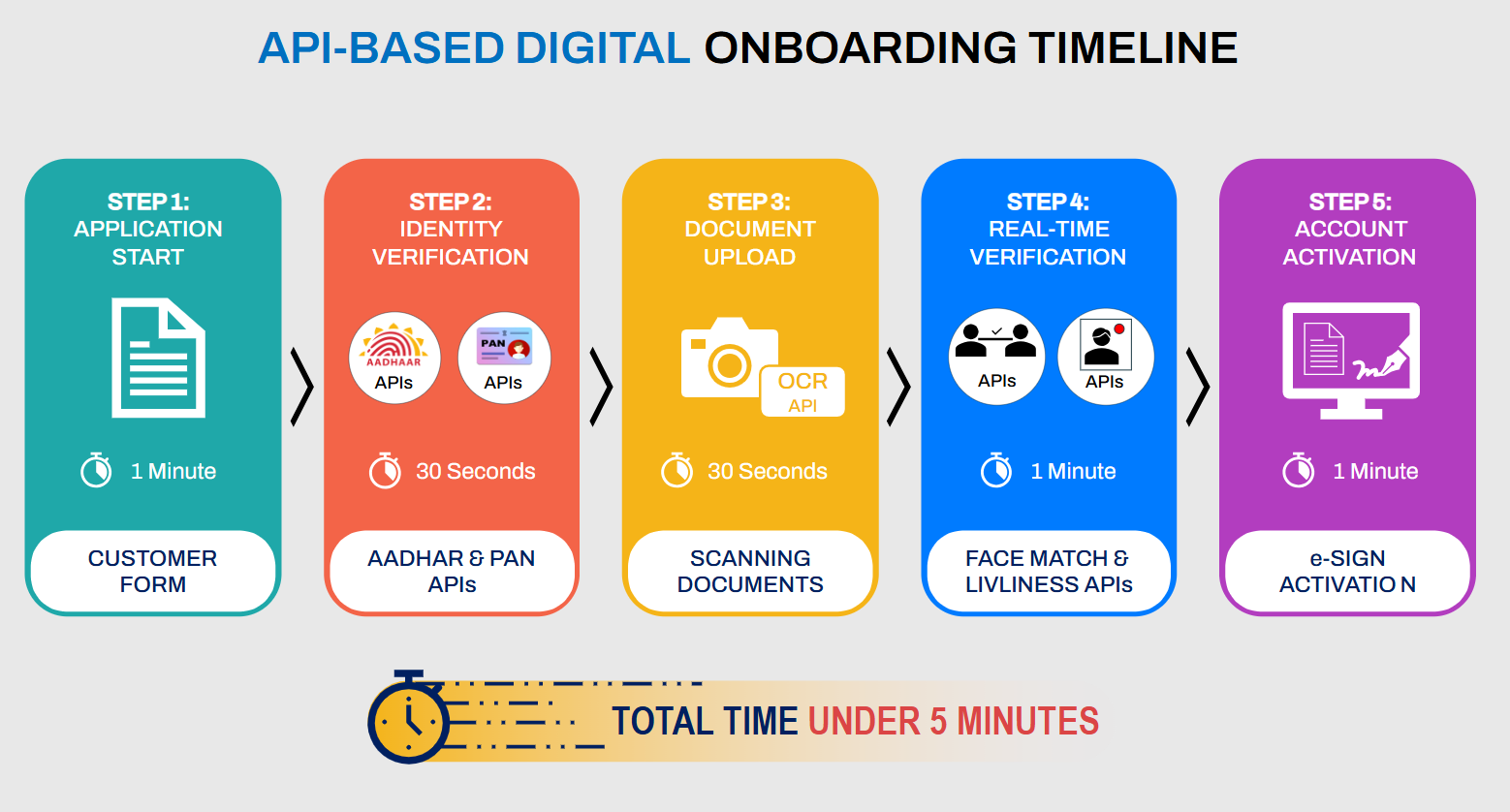

APIs have turned onboarding into something fast and user-friendly, cutting processing times by up to 85% so you can wrap it up in under five minutes from your phone. It also drives substantial cost reductions by eliminating paper handling and minimising staffing needs, while offering seamless scalability to manage high customer volumes without added resources.

Customers benefit from a smooth digital experience. Onboarding can now be done from anywhere via smartphone, with instant account activation and no branch visits are required. Digital journeys have also enhanced accuracy through Optical Character Recognition (OCR) and database validation, minimising errors and fraud.

How APIs Are Changing Customer Acquisition

Building on that digital pivot from paper-based KYC, APIs have supercharged how financial institutions attract and sign up new customers. During COVID-19, when physical bank branches were off-limits, mobile banking in India surged 99% from March 2019 to September 2021, while internet banking grew 18%.

Big banks jumped in with video KYC, letting you complete everything at home, auto-filling forms from Aadhaar, real-time checks via APIs, and e-signatures for instant approvals. RBI kept the momentum going with amendments to the Master Direction - Know Your Customer (KYC) Direction, 2016, that boost API-friendly tools like Business Correspondent-led verifications.

The result? Institutions that implemented this API-driven approach generally achieved speed, satisfaction, and growth. Making the onboarding journey API-based turned out to be a competitive edge that pulls in more users effortlessly.

Challenges in Implementing API Integration

Implementing APIs comes with significant challenges, particularly due to strict regulatory and data security requirements. Financial institutions manage highly sensitive transactional data, which demands enterprise-grade encryption, HTTPS protocols, and strict adherence to regulations such as the Prevention of Money Laundering Act (PMLA) and RBI guidelines.

Then there's integrating the traditional legacy systems, which demands middleware and upfront costs for infrastructure and expertise, particularly tough for smaller players. Technical mismatches in numerous data formats add complexity, and staying ahead of evolving regulation technology like data localisation requires constant vigilance.

Landmark Systems and Solutions: Your Partner in Digital Transformation

Landmark Systems and Solutions stands at the forefront of India's fintech revolution. Our dKYC API solution provides a comprehensive digital KYC and customer onboarding platform designed specifically for Banks and NBFCs.

Our API-driven solution dramatically reduces onboarding time while maintaining the highest standards of regulatory compliance and security. The platform seamlessly integrates with your existing core banking systems, supports both mobile and web applications, and enriches customer experience while reducing fraud.

With deep expertise in cloud platforms, we ensure robust and scalable infrastructure that handles peak demand efficiently. Our solution is specifically designed to address the latest RBI regulatory requirements, including the 2025 KYC amendments.

Ready to transform your customer onboarding experience? Visit www.lsssoftware.com to explore how our API-powered dKYC solution can accelerate your customer acquisition, ensure speed and security, and deliver exceptional user experiences.

The future of financial services is digital, and it starts with the right API integration strategy. To see a quick demo of our next-gen digital onboarding solution, talk with us today.

Official References

- RBI Master Direction on KYC, 2016 for regulatory compliance for banks and NBFCshttps://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11566

- Enforcement Directorate for Prevention of Money Laundering Act 2002https://enforcementdirectorate.gov.in/sites/default/files/Act&rules/THE%20PREVENTION%20OF%20MONEY%20LAUNDERING%20ACT,%202002.pdf

- UIDAI for Aadhaar Authentication and Offline Verification Regulations 2021https://uidai.gov.in/images/The_Aadhaar_Authentication_and_Offline_Verifications_Regulations_2021.pdf